Don’t go chasing unicorns

(or, how to support a more inclusive startup ecosystem)

Venture capital should never have become the standard way for us to fund new businesses. As an asset class, it’s uniquely designed to fund disruptive innovations. It does this by funding ventures that are likely to fail, but — if successful — can result in outsized outcomes. In other words, it’s a ‘home run’ based model. For a venture capitalist, seeing 6 or 7 out of 10 portfolio companies fail is part of the playbook. In fact, if VC’s aren’t seeing enough failures in their portfolio, they take it as a sign that they may not be taking enough risk (as Babe Ruth once said: “every strike brings me closer to my next home run”). Good VC’s understand they aren’t looking for a ‘normal distribution’ of outcomes in their portfolio — they’re looking for the “fund maker”. Or in other words, the unicorn.

But does that kind of failure rate represent a good deal for (most) founders? How about for society as a whole?

By looking at the world through a venture capital lens, we do three things that are often bad for founders, workers, communities and the planet:

- we overlook companies that could become good, sustainable businesses, but aren’t likely to generate the outsized returns the venture funds are seeking

- we make companies more likely to fail by pushing them to take on excessive risk in pursuit of a moonshot

- we push companies to ‘exit’, whether or not it allows them to stick to their founding vision and mission

In fact, it’s debatable whether VC is a great model for investors themselves. In general, only the elite ‘top quartile’ venture funds have generated what is often referred to as “venture returns” for their investors (the LPs). Unicorn hunting is a tough business!

There’s no need for me to rehash the failings of the VC model here. In their blog posts “Sex & Startups” and “Zebras Fix What Unicorns Break”, Jennifer Brandel, Astrid Scholz, Aniyia Williams and Mara Zepeda brilliantly articulate how our obsession with VC, exits and unicorns is getting in the way of building good, sustainable, mission-driven businesses led by diverse founders. They proposed an alternative company model — the Zebra — which would renounce the winner-take-all, exit-focused paradigm in favor of a sustainable, profitable, stakeholder-driven one. As they point out, this is not just about funding ‘lifestyle businesses’ that aren’t ‘VC backable’. It’s about creating an alternative economic model where value and wealth are more equitably and broadly distributed (instead of accruing to the privileged few investors who have the luck, insight and access to put some money into companies like Facebook, Uber etc.).

At Candide Group we seek to invest in companies and funds that offer systemic solutions to social justice and sustainability issues. But we also understand that the economic model, as well as the investment tools, need to be an inseparable part of how we think about systemic change — simply applying the same old models to companies that are serving low-income customers or building green products just isn’t going to cut it. We believe HOW businesses operate is every bit as important as WHAT product or service they’re selling. And investment structures — who owns the business, what does an exit look like, who makes decisions etc. — are an incredibly powerful lever in defining that HOW.

In “Sex & Startups”, the Zebra leaders posed a challenge to the finance community — how can we fund and support these types of businesses?

“Outside of bootstrapping, or relying on wealthy friends or family, or having connections to the limited network of mission-driven angel investors, there’s a dearth of options for tech companies seeking financing: It’s venture capital or bust. So what are founders like us to do? Where do we go from here?”

Below is an attempt to suggest very specific answers to that question. This could get a bit wonky and technical, but will hopefully contribute to the conversation toward creating new structures and funds to support businesses that share this ethos (“Zebra Funds” if you will).

Revenue-based financing to the rescue?

Revenue-based financing has gained some popularity as an alternative to VC. A company agrees to pay out a % of its top-line sales, usually until its investors achieve some pre-determined return. As an example, company ABC raises $500,000, and in return pays out 3% of its sales until investors have received a total of $1,000,000 in distributions (a 2x return on their $500,000 investment). [1]

This model is appealing for various reasons:

- Investor and company interests are aligned: if the company grows quickly, investors earn a quick return (and high IRR); but if the company is growing slowly, it may take a very long time for investors to recover their investment. This is unlike traditional debt, where interest/principal payments are fixed regardless of how well the company does.

- Fewer ’strike outs’ for investors: a company doesn’t have to scale and exit to generate a return, since distributions are happening throughout the growth of the company. With fewer ‘zeros’ in the portfolio, investors don’t have to chase home runs.

- No pressure to sell the business: liquidity is structured into the investment, so founders are free to decide whether they want to sell the business or not.

- Relatively simple: these can be very simple legal documents. Investors often like revenue-based payments since it’s very easy to define ‘revenues’, whereas profit-based payments require a lot more oversight around how ‘profit’ should be defined in any given year.

But not so fast

At Candide Group, we like revenue-based financing for all the reasons above, and have used similar structures in a couple of our investments. But we have also come to realize this model only works in a pretty limited set of circumstances. Revenue-based financing is more typically used in the context of later stage businesses.[2] It turns out that adapting this as a tool for early stage investing often just doesn’t work.

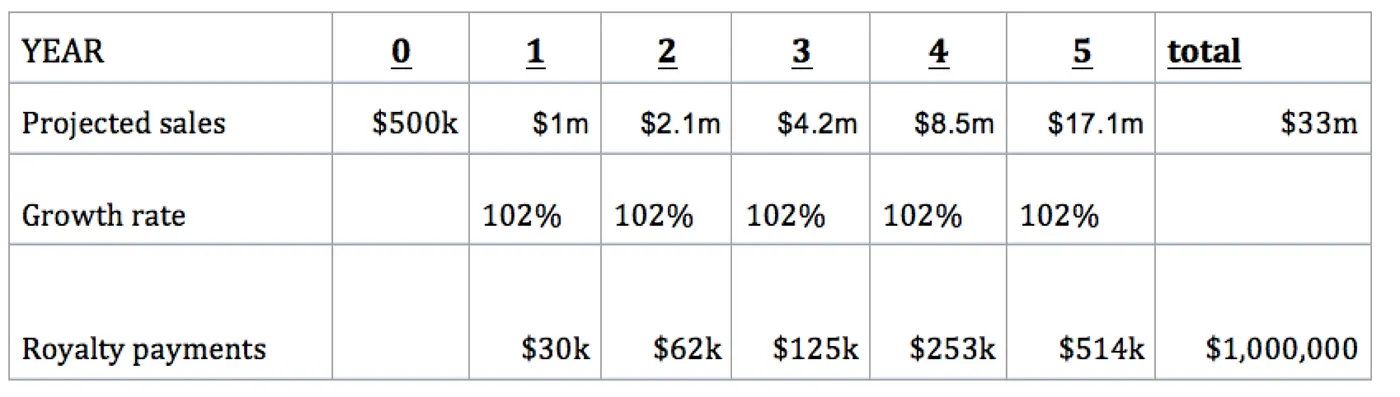

Take the example we used above: a company that takes on a $500,000 investment and then pays out 3% of sales would need to generate $33m in sales, over the life of the investment, in order for investors to get their 2x return ($33.3m * 3% = $1m). For an early stage business, that might imply a pretty ambitious growth trajectory. Say the company is currently generating about $500,000 in annual sales. It would have to more than double its revenues every year for 5 years in order to reach $33m in cumulative sales over a 5 year period:

Note: See Disclaimer for information about hypothetical data

To make the math even harder, many (in fact, most) investors would argue that a 2x return would be too low when investing in an early stage business. Knowing that some investments may still fail, even under this more conservative model, they would more likely require a 3–5x return on their investment. For investors to achieve a 3x return on their $500,000 investment, the company would need to generate $50m in sales over the life of the investment ($50m*3%=$1.5m). This would imply roughly 125% annual growth over 5 years, or 75% annual growth over 7 years.

And, what if the company needs to raise more than $500,000? If a company is raising $1m, and investors are seeking a 2x return on investment, the company would have to generate $66.6m in sales while paying out 3% of sales as before (3%*$66.6m = $2m).

At some point, the growth trajectory required to repay investors starts to look a lot like the kind of ‘hockey stick’ projections that the venture capitalists are looking for. And if investors are buying into the venture-style growth, they should probably pause and wonder why they’re targeting a 2x return instead of the 10x outcome venture investors are chasing.

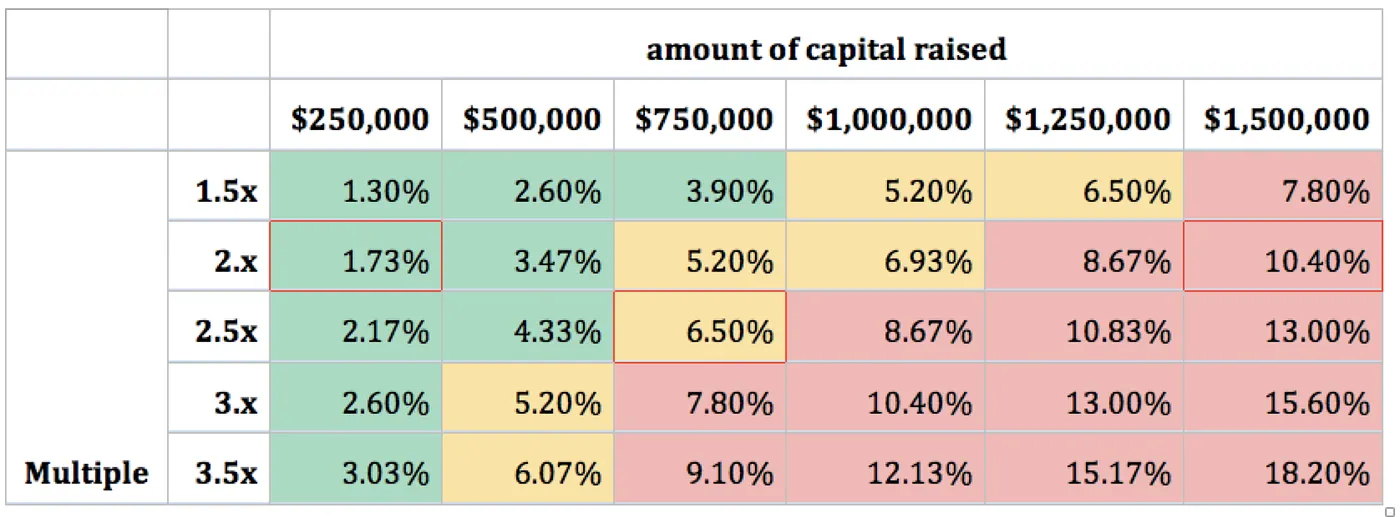

Overall, the more capital the company needed and/or the higher the return investors demand, the harder it gets to make the numbers work. Either the company has to hit unrealistic growth rates, or it has to pay out an unrealistic % of revenues to investors. The table below summarizes how and when the math breaks down:

Note: See Disclaimer for information about hypothetical data

The numbers in the table above are for a company generating $750,000 in annual sales at the time of the capital raise, and assuming an 80% annual growth rate over the next 5 years (pretty respectable growth rates!).

What do the numbers mean? Take three examples (cells outlined in red):

- If the company is raising just $250,000 and investors are looking for a 2x return on capital, the company would just need to pay out 1.73% of sales over 5 years (color coded green because that would be very manageable)

- If the company is raising $750,000 and investors are looking for a 2.5x return, the company would have to pay out 6.5% of sales over 5 years to repay investors. Color coded yellow because this could be hard for the company to manage, but could work if stretched out over more years

- If the company is raising $1.5m and investors are looking for a 2x return, the company would have to pay out 10.4% of revenues (color coded red since this would be much too big of a burden for the business)

What this simple math tells us is that a revenue share deal would rarely work if a company is trying to raise more than, say, $750,000. Of course, the picture gets even worse (more red cells) if the business was starting from a lower base (e.g. $500,000 in annual sales instead of $750,000) and/or if it were growing at a slower pace (e.g. 50% year over year instead of 80%).

In general, for early stage businesses, revenue-based finance really only works if you need a relatively small amount of capital, say $500k or less.

But what do we do about all those business that need, $1m, $3m or more to get to a healthy and sustainable scale? They mostly fall in a no man’s land — too big for a revenue share deal, but too small of an outcome for most venture funds to care.

Redemption

A tool that we believe is highly useful and underutilized is the equity buyback, also known as equity redemption.

Instead of taking money out of the business through revenue-share distributions, investors buy shares and hold them until the company is profitable enough. What does ‘enough’ mean in this context? Enough to buy the investors out, using a combination of available cash and/or new capital. Essentially, once the company is profitable, it can access lower cost of capital (typically debt) and use that to refinance its original investors.

The obvious question here is at what price should the shares be redeemed? There are several ways to determine that:

- The original investment could specify a minimum return (e.g. a 15% IRR, or 2x return)

- The redemption price could be determined based on a revenue or EBITDA multiple (e.g. 2x sales at the time of redemption)

- A third party valuation could be done to determine fair market value

Let’s consider an example:

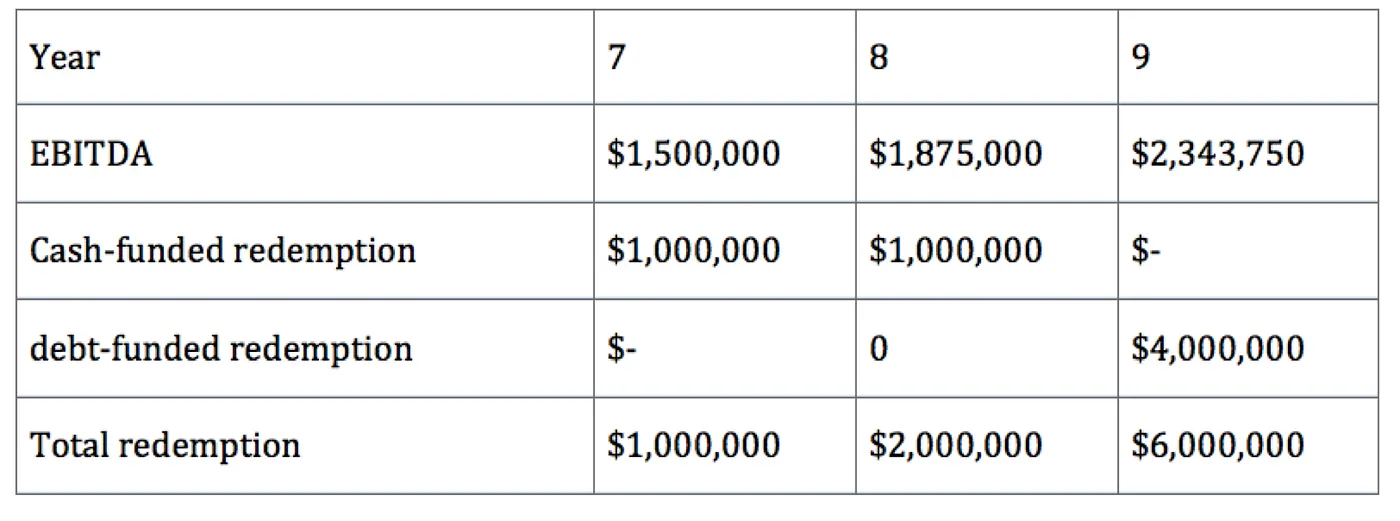

Company XYZ raises $2m in preferred equity in exchange for 40% of the company, with a redemption option at year 7. The redemption option specifies that investors can put the shares back to the company with a minimum return of 3x.

At the time of the investment, the company is generating $1m in annual sales and is almost profitable, and 7 years later it is generating $10m in sales and $1.5m in EBITDA. (note: in this example, the company raised 4x as much capital than the company in our revenue-share example, and took almost twice as long to reach $10m in sales. For most companies, this is probably a more realistic rate at which they’d convert investment dollars into growth).

Knowing that the founders don’t intend to sell the business, the investors decide to initiate a share redemption in year 7. Based on the 3x minimum return, shares will be repurchased at a price that results in a $6m return to investors.[3]

Where would the $6m come from? The company could fund part of the redemption using cash, but now that it is profitable is can also take on some debt. Management and the investors agree on a 3-year process to enable the company to generate enough EBITDA to support the $6m payout. It could look something like this:

Note: See Disclaimer for information about hypothetical data

This structure has a couple of clear benefits vs. the revenue share structure we considered above:

- Investors are not taking money out of the company during the crucial early years of growth, and instead are reinvesting into the business.

- this model can be applied to larger investments. If we tried to apply our revenue-share model to the company in this example, we would have had to extract more than 10% of revenues over 9 years to get the same 3x return (which would have completely strangled the company)

For the redemption model to work companies generally need to strive for profitability and avoid raising too much capital along the way. If instead of raising $2m it had raised $5m, it would have been very hard for investors to generate a return. Ideally, the capital being raised should be the catalyst that gets the company onto solid footing (profitability).

Building a portfolio

Investors too have to shift their mindsets. A venture fund predicated on 10x home-runs just wouldn’t plan around this outcome or consider this a success. A fund using this strategy would need to be more conservative and avoid taking on too much risk.

Fund managers who think this way can be counted on far too few fingers. One that we’ve learned a lot from and has applied this approach successfully is InvestEco, a venture fund based in Toronto and investing in sustainable food businesses. Using a redemption structure, InvestEco has been able to successfully support (and exit!) businesses that don’t fit the ordinary venture playbook such as Organic Meadow (a dairy co-op) and Horizon Distributors (an organic distributor). And its portfolio includes other regional or mid-sized businesses that wouldn’t fit in a traditional venture portfolio, such as 100km Foods (an organic distributor), Mama Earth Organics (direct to home retailer of organic food) or Rowe Farms (a regional retailer of locally grown food).

Using this structure simply enables InvestEco to support a broader range of business; not just the ones that look like a potential VC home run. A venture fund tied into its existing ‘home run’ model can’t just decide it makes a couple of investments like this. It would be directly at odds with their fund model. But applying this strategy across a portfolio could very well lead to strong competitive returns by way of a very different distribution.

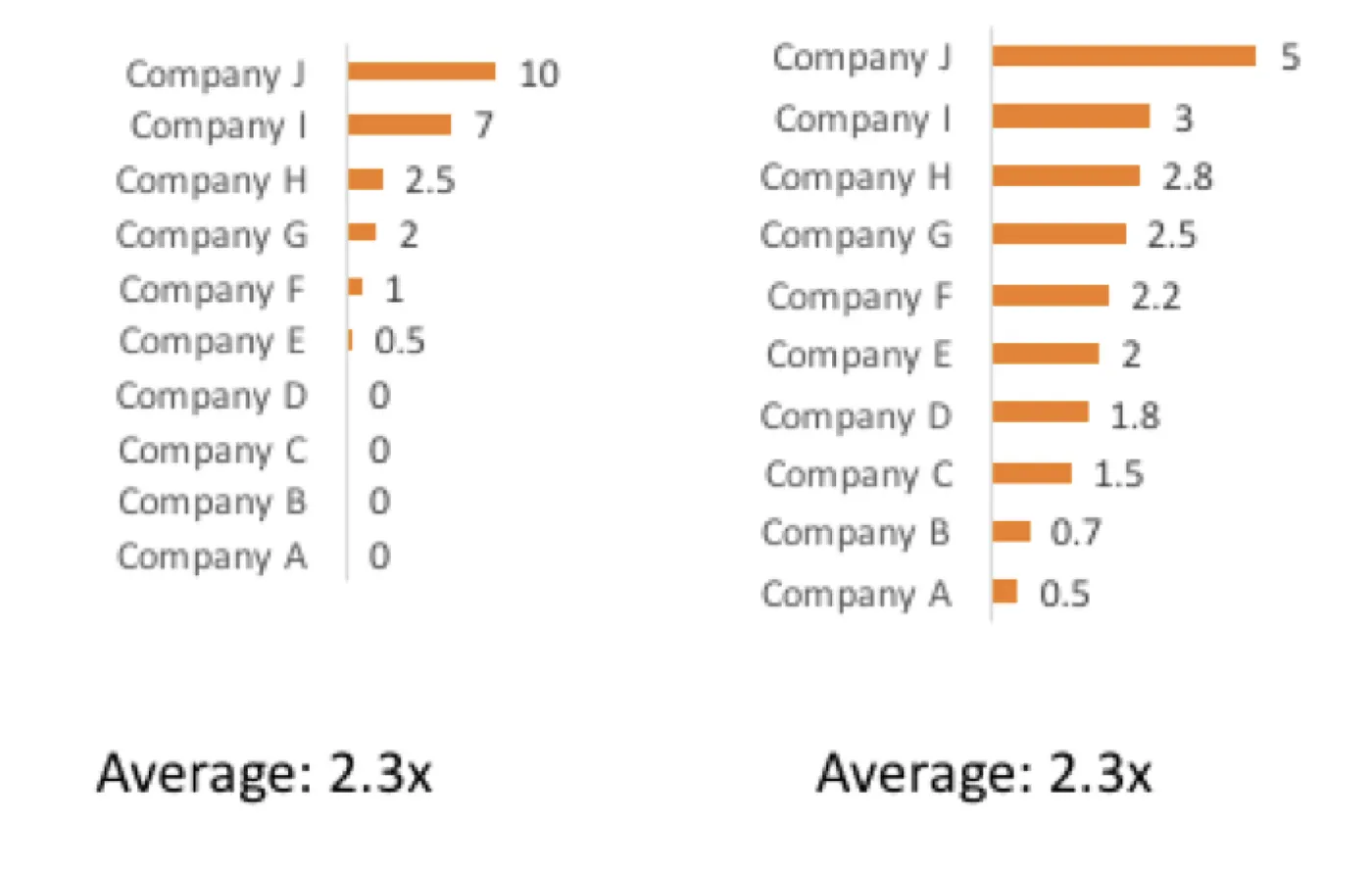

Consider the simplistic, hypothetical example below, showing two very different ways to build a portfolio generating a strong 2.3x return for investors.

On the left is a VC portfolio, where 6 out of 10 companies fail, 2 do really well and 2 do ok. One the right is a zebra portfolio, where only 2 out of 10 companies fail, 1 delivers a very strong 5x return and the remaining 7 are what VCs might consider ‘singles’ or ‘doubles’:

Note: See Disclaimer for information about hypothetical data

Onwards

We need many more funds to think this way if we’re going to enable the creation of more independent, diverse, mission-driven and sustainable companies. More zebras, as it were.

And it has to happen at the fund, or portfolio, level.

We’re seeing a groundswell of interest on the entrepreneur side, where more and more founders are realizing they shouldn’t jump on the venture capital treadmill. We have some catching up to do on the investor side, but a few innovators are emerging, such as InvestEco, Indie.vc and Purpose. Major funders are starting to pay attention as well. The Inter-American Development Bank, Rockefeller Foundation and Transform Finance released a helpful report on innovations in financing structures for social enterprises. MacArthur Foundation and others helped fund a handy open-source tool called the Impact Terms Project which compiles innovative financing tools.

We plan to collaborate with these early innovators, while also working closely with founders in co-designing and creating additional vehicles.

If you are an investor or founder who sees the need for more of this thinking, we invite you to join the conversation.

[1] Tweaks can be made to this basic model, such as (1) including a grace period (e.g. payments only start after a number months/years, or once the company hits a certain revenue threshold), (2) using some profit line instead of revenues (e.g. % of free cashflow, EBITDA etc.), or (3) instead of a revenue-based loan, the same % of revenues can be used to buy shares back from investors at a pre-determined price

[2] For example, mezzanine funds often use a revenue share as a ‘kicker’ on top of their fixed debt coupon.

[3] This is roughly equivalent to a 15% IRR for investors

This story is published in Noteworthy, where 10,000+ readers come every day to learn about the people & ideas shaping the products we love.

Follow our publication to see more product & design stories featured by the Journal team.